Everyone wants to know the best tax strategy, but that's usually the wrong place to start. Over the years, I've watched entrepreneurs chase deductions, form LLCs, elect S corporation status, and invest in real estate, all with the goal of keeping more of what they earn. Those are all smart moves, but on their own, they're just individual strategies. If your business, investments, and estate plan aren't working together, you're limiting the effectiveness of every one of them. Tax planning isn't about collecting more tools. It's about creating a structure where every financial decision supports the next one.

After more than 25 years working with business owners and investors, I've noticed something. The people who build lasting wealth aren't constantly searching for the next tax trick. They have a coordinated plan. Their legal structure supports their tax strategy. Their investments fit into their estate plan. Every piece has a purpose, and every decision reinforces the next. That's why I created The Trifecta®. It isn't another tax strategy or legal document. It's the framework that brings your business, investments, and estate plan together into one coordinated system designed to lower taxes, protect assets, and build long-term wealth.

The Trifecta Is More Than a Tax Strategy

A lot of people hear me talk about The Trifecta and assume it's a single strategy or a checklist of things to do. It isn't. It's the system behind every strategy I recommend.

Think about it this way. Forming an LLC doesn't automatically create a great tax plan. Electing S corporation status doesn't guarantee you'll save money. Creating a trust doesn't mean your estate plan is complete. Each of those tools serves a purpose, but none of them reaches its full potential when it operates on its own.

The Trifecta brings those pieces together. It coordinates your personal life, your investments, and your business so they function as one integrated system instead of three separate plans.

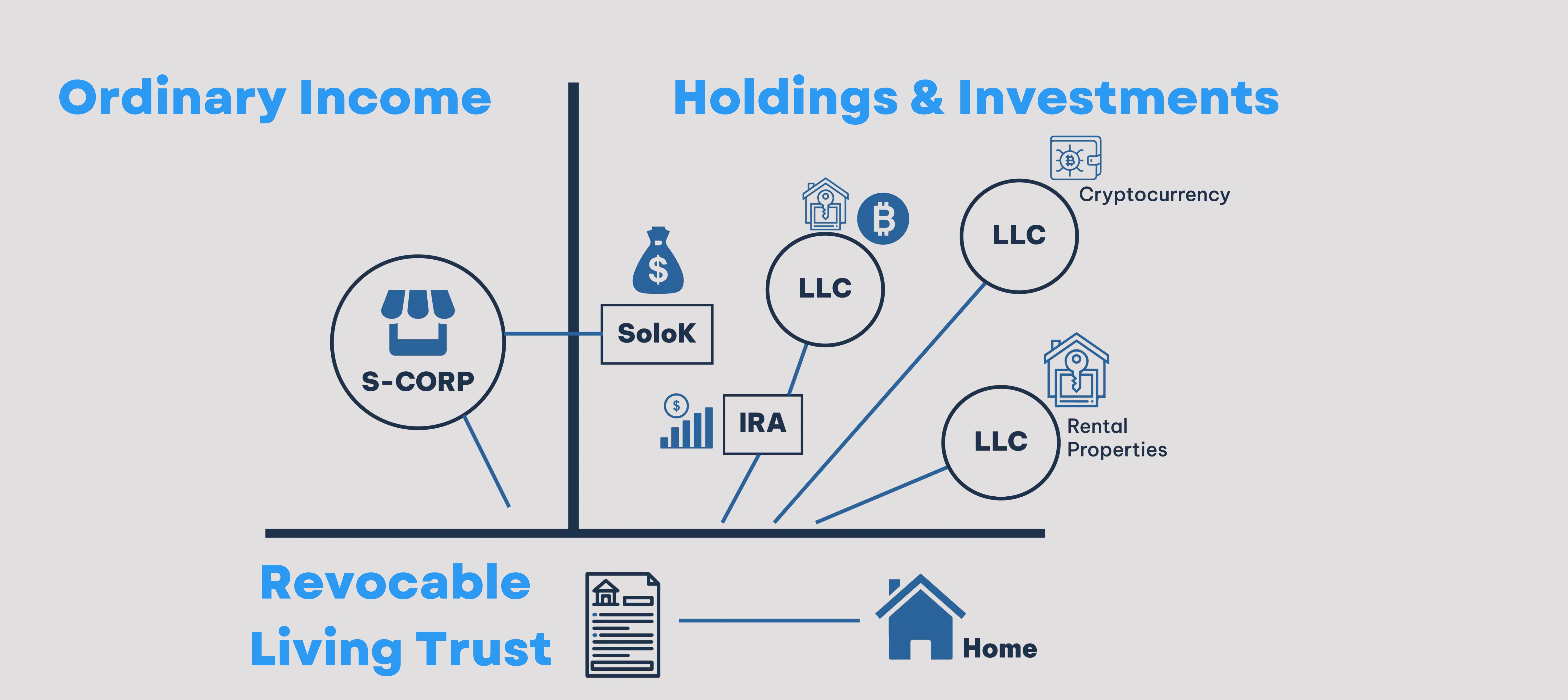

At its core, The Trifecta is built around three areas:

- The foundation: Your Revocable Living Trust

- Your holdings and investments: Rental properties, crypto, brokerage accounts, and other assets

- Your ordinary income: Your LLC, S corporation, or side hustle

Every financial decision should strengthen one or more of these areas, but more importantly, it should strengthen the relationship between them.

The Foundation: Your Revocable Living Trust

Whenever I introduce The Trifecta, I start with the foundation because that's exactly what a revocable living trust is. It isn't designed to save taxes. It isn't an investment vehicle. Its purpose is to create order and continuity for everything else you own.

A revocable living trust allows your assets to pass according to your wishes while helping your family avoid probate. It provides privacy, keeps your estate organized, and makes life much easier for the people you leave behind. That's valuable whether your estate is worth $200,000 or $20 million.

The trust also creates a natural home for your ownership interests. Instead of having LLCs, investments, and other assets scattered across different ownership structures, everything can work together under one coordinated estate plan. That's why I consider the trust the foundation of The Trifecta. Without a strong foundation, everything built on top of it becomes harder to manage.

The Right Side: Holdings & Investments

The right side of The Trifecta focuses on the wealth you're building outside your business. This includes rental properties, cryptocurrency, brokerage accounts, private investments, and other assets that grow your net worth over time.

These investments deserve just as much attention as your business because they're often where long-term wealth is created. They're also where many people unknowingly expose themselves to unnecessary risk.

For example, rental properties generally shouldn't be owned in your personal name. Holding them in properly structured LLCs can help separate liabilities, simplify ownership, and better protect the rest of your assets if something goes wrong. The goal isn't simply to own real estate. The goal is to own it in a way that supports both your asset protection and your long-term estate plan.

Too often I meet investors after they've already accumulated several properties and are trying to reorganize everything later. That's usually much harder than building the right structure from the beginning.

The Left Side: Your Ordinary Income

For most entrepreneurs, the left side of The Trifecta is where the excitement begins because this is where many of the biggest tax planning opportunities exist.

Your business gives you options that simply aren't available to W-2 employees. An LLC can provide liability protection. An S corporation election can reduce self-employment taxes when the numbers make sense. Business deductions, retirement plans, and strategic compensation planning can all help you legally keep more of what you earn.

Where people get into trouble is treating those strategies as individual solutions instead of pieces of a much larger system. I see business owners rush to elect S corporation status because they heard it saves taxes, even though they haven't addressed the rest of their structure. That's backwards.

An S corporation isn't the strategy. It's one tool within the strategy. When your business structure supports your investment plan, your estate plan, and your overall tax strategy, that's when the real benefits begin to compound.

The Power Isn't in the Pieces. It's in How They Work Together.

This is where I see a lot of business owners miss the bigger picture. They check all the boxes. They form an LLC. They create a trust. They elect S corporation status. Maybe they even purchase rental properties in separate entities. On paper, everything looks great.

The problem is that simply having those pieces doesn't mean you have a strategy.

The real value comes from how those pieces work together. Your business should support your investment goals. Your investments should fit into your estate plan. Your tax strategy should influence how your entities are structured. Every decision should complement the others instead of existing on its own. That's the difference between having a collection of legal documents and having a coordinated wealth-building system.

When someone asks me whether they need an LLC, an S corporation, or a trust, my answer is usually the same: it depends on how it fits into the rest of your plan. I rarely look at one piece in isolation because every recommendation affects something else. That's exactly what The Trifecta is designed to solve.

Every Financial Decision Should Support Three Goals

One of the easiest ways to think about The Trifecta is to ask yourself three simple questions whenever you're making an important financial decision.

1. Will this help lower taxes?

2. Will this improve asset protection?

3. Will this help build long-term wealth?

The best decisions accomplish all three.

Let's use a simple example. Imagine you're buying your first rental property. Most people immediately start thinking about financing or finding tenants. Those things are important, but I also want to know who should own the property, whether an LLC makes sense, how it fits into your estate plan, and what tax opportunities it creates. Instead of making one isolated decision, you're making several coordinated decisions that strengthen your overall financial picture.

The same is true when starting a business, opening a retirement account, or purchasing another investment. The individual strategy matters, but it matters even more when it's supporting everything else you're trying to accomplish.

Don't Chase Strategies. Build a System.

It's easy to get distracted by the latest tax strategy or social media trend. Every year there's a new deduction, a new planning technique, or a new entity structure that promises to save thousands of dollars in taxes. Those strategies may be perfectly legitimate, but they're rarely the place to start.

I've always believed that structure comes before strategy. When your legal entities, investments, estate plan, and tax planning are properly coordinated, you'll naturally uncover opportunities to reduce taxes and protect your assets. Without that foundation, you're constantly trying to force individual strategies into a structure that wasn't designed to support them.

That's why I encourage business owners to spend less time asking, "What's the newest tax strategy?" and more time asking, "Is my overall structure working the way it should?" That one question usually leads to much bigger opportunities.

The Trifecta Grows With You

One of the things I love most about The Trifecta is that it isn't just for someone running a large company or managing a substantial real estate portfolio. It's a framework that grows with you throughout every stage of your financial journey.

Maybe today you have a side hustle and one rental property. Five years from now you may own multiple businesses, several investment properties, and a much larger investment portfolio. The strategies will evolve as your situation changes, but the framework stays the same.

That's why I don't view The Trifecta as a one-time project. It's something you revisit as your business grows, your investments expand, and your family's needs change. Every major financial milestone is an opportunity to make sure all three areas are still working together.

When that happens, you're not constantly rebuilding your plan. You're simply strengthening a system that's already in place.

The Bottom Line

If there's one thing I hope you take away, it's that no single tax strategy will ever outperform the right structure. An LLC by itself isn't enough. An S corporation election isn't enough. A trust isn't enough. The real advantage comes when those pieces work together. The Trifecta is the framework behind every recommendation I make because it recognizes that no financial decision exists in a vacuum.

That's exactly what we help entrepreneurs build every day at KKOS Lawyers. We don't just form LLCs or draft trusts. We create a coordinated legal and tax strategy that's tailored to your business, your investments, and your long-term goals, so every piece of your financial life is working together instead of independently.

The sooner your structure is in place, the sooner every future tax strategy has a stronger foundation to build on.

.png?width=6440&height=1438&name=KKOS%20Book%20a%20Call%20(2).png)

Trifecta FAQs

Do I really need a trust if I’m not rich?

Yes! A trust isn’t just for the wealthy. It helps avoid probate, keeps your estate organized, and protects your family from legal battles and delays.

At what income should I convert my LLC to an S corp?

As soon as you’re netting $50,000 or more per year. That’s where the self-employment tax savings kick in.

What’s the difference between an LLC and an S corp?

An LLC is a legal structure. An S corp is a tax status. You can convert your LLC to be taxed as an S corp—best of both worlds.

Do I need separate LLCs for each rental property?

That depends on how much equity each property holds. A good rule of thumb: if a property has over $200K in equity, consider its own LLC.

Can my trust own my LLCs and S corps?

Yes! In fact, it should. That’s how you keep everything connected and organized under the Trifecta.