Starting a business with a partner can be one of the smartest decisions you'll ever make. It can also become one of the most expensive mistakes if you don't set it up correctly from the beginning. I love partnerships. I've built multiple successful businesses with partners over the years, and I've seen firsthand what makes them work. If you're forming an LLC with a partner, this isn't the time to cut corners or download a generic operating agreement online. Doing it yourself can create problems that last for years.

Don't Treat a Partnership LLC Like Any Other LLC

I understand why people file their own LLCs. If you've started a business before, maybe you've completed the paperwork yourself or used an online filing service. There are situations where that's perfectly reasonable. A partnership is not one of them.

I've said it before and I'll say it again: a DIY partnership LLC is a lawsuit waiting to happen. The reason is simple. When you own an LLC by yourself, most of the legal documents are about protecting you and organizing your business. The moment you add another owner, everything changes. Now you're dealing with two families, two sets of financial goals, two personalities, and two different memories of what was supposedly agreed upon.

That's why your LLC operating agreement becomes one of the most important documents you'll ever sign. It doesn't just define ownership. It answers the questions you haven't thought to ask yet, and the ones you'll wish you'd answered when things don't go according to plan.

Think Beyond Today

When people form a partnership, they're usually focused on getting the business off the ground. Everyone is optimistic. Everyone is excited. Nobody wants to think about what happens if something goes wrong. That's exactly why you need to.

One of the first conversations I want partners to have has nothing to do with making money. It has everything to do with what happens if one of you isn't around anymore. Who inherits the ownership interest? Does your partner suddenly become business partners with your spouse? Your children? Your parents? An ex-spouse after a divorce?

I've seen business owners spend years building a successful company only to discover they never planned for what would happen if one partner died unexpectedly. Now the surviving partner is trying to run the business while negotiating with family members who never intended to own part of the company.

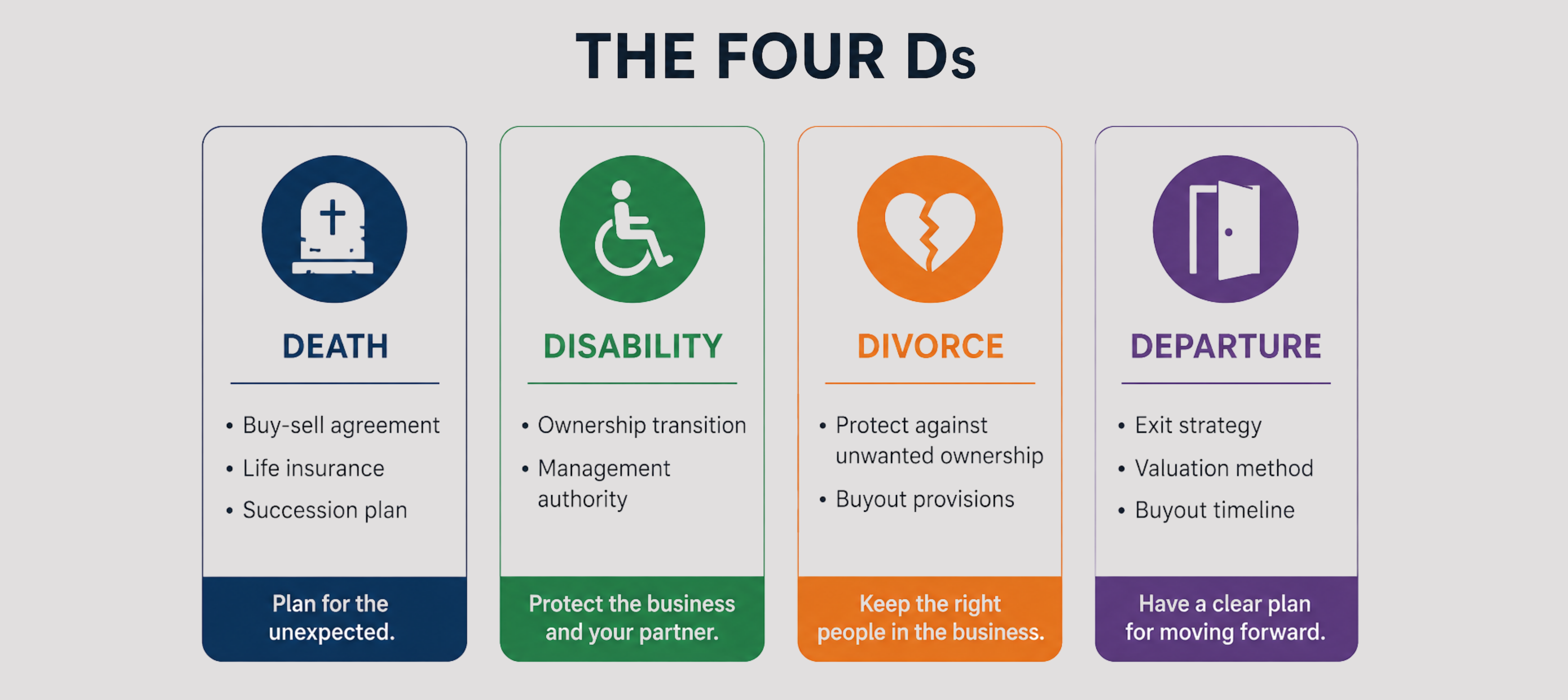

This is where a properly drafted buy-sell agreement becomes invaluable. In many cases, we build buy-sell provisions directly into the LLC operating agreement so there's already a roadmap for what happens if a partner dies, becomes disabled, gets divorced, or simply wants to leave the business.

I call these the Four Ds:

- Death

- Disability

- Divorce

- Departure

None of these situations are fun to think about, but every one of them can happen. Having a plan before they do can save friendships, businesses, and families.

Make Sure Your Ownership Fits Into Your Overall Plan

Another issue that gets overlooked is how the partnership fits into your broader legal and tax structure. For example, if the partnership owns rental real estate, your revocable living trust will often be the appropriate owner of your LLC interest. If it's an operating business, your ownership may be held by your S corporation instead. The right answer depends on the role that business plays within your overall structure.

This is where I always come back to the Trifecta. Your entities shouldn't exist in isolation. They should work together with your tax planning, asset protection, retirement strategy, and estate plan as part of one coordinated system.

Too many business owners set up an LLC without asking how it fits into everything else they own. Then years later they're trying to untangle ownership issues that could have been avoided from the start.

Good Partnerships Need Good Tax Planning

A lot of attorneys can draft an operating agreement. Far fewer understand how the tax planning fits into it. That's a problem because the way you structure a partnership can have a significant impact on your tax strategy.

For example, if you're operating a business together, one of the most common mistakes I see is making an S corporation election at the partnership level. In many cases, the better approach is for each partner's own S corporation to own their partnership interest, not for the partnership itself to become an S corporation.

Retirement planning is another area that deserves attention. One partner may want to maximize retirement contributions while the other needs more cash flow today because they're paying for college tuition or raising a young family. Those conversations should happen before the documents are signed, not years later after everyone discovers they're working toward different goals.

Then there's the issue of distributions. What happens if the business is profitable, but one partner wants to leave all the money in the company while the other needs cash to pay the taxes on their share of the income? That's called phantom income, and it's one of the fastest ways to create frustration between partners. Even if the business doesn't distribute cash, each partner may still owe tax on their share of the profits. Your operating agreement should establish a clear process for handling distributions so nobody gets stuck paying taxes without receiving any money.

Define Roles Before the Work Begins

One of the healthiest conversations partners can have is deciding exactly who is responsible for what. That sounds simple, but it's often where partnerships begin drifting apart.

Maybe one partner is contributing most of the startup capital while the other is responsible for running the business every day. Those aren't the same roles, and they shouldn't necessarily come with the same authority.

Consider…

- Who's responsible for daily operations?

- Who can sign contracts?

- Who can hire employees?

- Who approves major purchases?

- What happens if the business needs another $50,000 next year? Does each partner contribute equally, or is one partner expected to provide additional capital?

The clearer these expectations are from the beginning, the fewer misunderstandings you'll have later.

I've also seen plenty of 50/50 partnerships discover that equal ownership doesn't automatically solve disagreements. In fact, it can create deadlocks if the partners don't have a process for resolving major decisions.

Sometimes that means requiring unanimous approval for significant transactions. Sometimes it means bringing in a trusted third party to break a tie. The solution depends on the business, but the important thing is deciding before you're in the middle of an argument.

Talk About the Exit Before You Even Build the Business

Most partnerships begin with excitement. Very few begin by talking about how they'll eventually end. That conversation matters.

If you're buying an investment property together, when will you sell it? If you're building a company, is the goal to own it forever or eventually sell it? What happens if one partner wants out five years from now and the other wants to keep going?

I've watched partners spend months arguing over an exit because each person remembered the original plan differently. One thought they were building a long-term business. The other thought they were creating something to sell. Putting those expectations into writing eliminates a lot of unnecessary conflict. Even if the plan changes later, you'll have a starting point everyone agreed to.

Be Careful When Raising Money

One final warning. Be very careful about calling someone an "investor." There's a big difference between a partner, a lender, and an investor, and those distinctions matter legally.

Once you begin raising money from passive investors, you're entering an entirely different legal landscape that can involve securities laws and regulations. That's not something to figure out after you've accepted someone's check.

If your business plan includes raising capital, make sure you're working with an attorney who understands both business entities and securities compliance before moving forward.

The Bottom Line

The strongest partnerships aren't built on trust alone. They're built on clear expectations.

Every successful partnership I've been part of involved difficult conversations at the beginning. We talked about responsibilities, decision-making, taxes, succession planning, ownership, and exit strategies before they became problems. Those conversations weren't always easy, but they were a lot easier than trying to sort everything out after a disagreement.

If you're thinking about starting a business with a partner, don't settle for a generic operating agreement or an online filing service. A well-structured partnership should protect both the business and the people behind it.

If you're forming a partnership LLC or want to review an existing operating agreement, KKOS Lawyers can help build a structure that's designed for both legal protection and long-term tax strategy. Getting it right from the beginning is always less expensive than fixing it later.

.png?width=6440&height=1438&name=KKOS%20Book%20a%20Call%20(2).png)