If you've followed me for any period of time, you know I'm a big believer in Roth accounts. I love building tax-free buckets because I love giving people more flexibility later in life. That's exactly why I like the Mega Backdoor Roth. It isn't some secret loophole or magic retirement account. It isn't for everyone, but for the right investor with the right retirement plan, it's alive, well and one of the most powerful ways to move significantly more money into tax-free accounts.

What Is a Mega Backdoor Roth?

The Mega Backdoor Roth isn't a special retirement account you open. It's a strategy. More specifically, it's a combination of retirement planning strategies that allows you to move substantially more money into Roth accounts than most people think is possible.

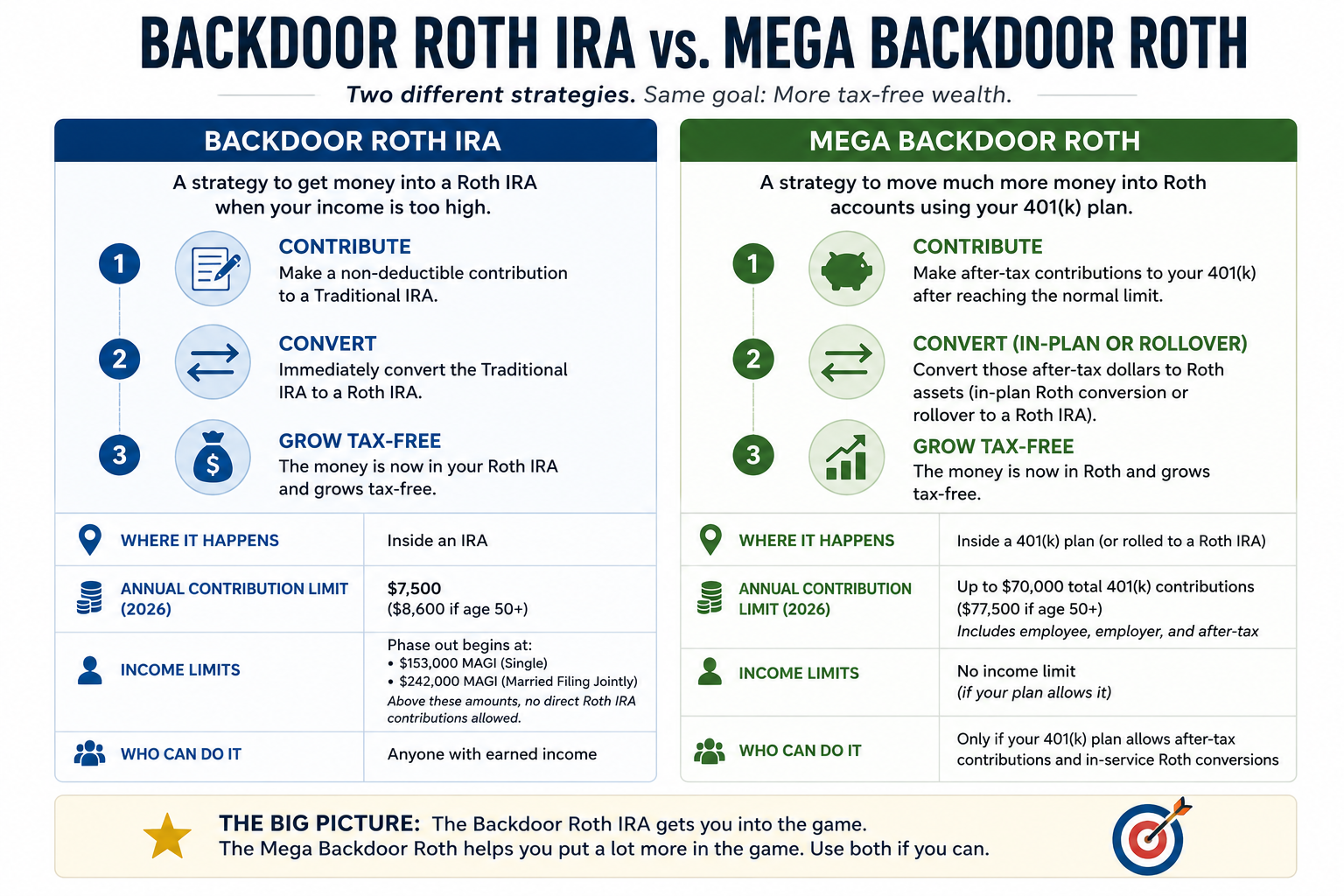

A lot of investors are familiar with a Backdoor Roth IRA. That's the strategy high-income earners use when they exceed the Roth IRA income limits. For 2026, direct Roth IRA contributions begin phasing out at modified adjusted gross incomes of $153,000 for single filers and $242,000 for married couples filing jointly. Once your income exceeds those limits, the Backdoor Roth IRA often becomes the next conversation.

The Mega Backdoor Roth is different. Instead of working around IRA contribution limits, it uses specific features inside a qualified 401(k) plan to convert after-tax contributions into Roth dollars. That's why it's called "mega."

The goal isn't simply making bigger retirement contributions. The goal is building a much larger source of tax-free wealth over time.

Is the Mega Backdoor Roth Still Allowed?

Yes. Despite what you've probably seen on YouTube or social media, the Mega Backdoor Roth is alive and well.

Several years ago, Congress considered legislation that would have eliminated both the Backdoor Roth and Mega Backdoor Roth strategies, but those provisions were never enacted. Those proposals never became law. More recently, I've seen people confuse the old Build Back Better proposal with the One Big Beautiful Bill that was signed into law. They're completely different pieces of legislation.

The bottom line is simple: don't assume a strategy disappeared because someone without tax credentials made a video claiming it did. Tax law changes constantly, which is why it's important to verify information before assuming you've lost a valuable planning opportunity.

This Isn't Where I Tell People to Start

Whenever someone asks me about the Mega Backdoor Roth, I usually answer their question with another question. Have you already built a solid retirement foundation?

I like to see people take advantage of the basics before moving into more advanced strategies. That usually means contributing enough to your employer's 401(k) to receive the full company match, funding your Roth IRA or completing a Backdoor Roth IRA if your income is too high, maximizing an HSA if you're eligible, and making sure you're using the right retirement plan for your business if you're self-employed.

If you're married, I also want to make sure you're thinking beyond your own retirement account. Can your spouse be contributing? If your children have earned income, have you considered funding a Roth IRA for them? Have you looked at education planning opportunities like a Coverdell ESA?

That's why I don't present the Mega Backdoor Roth as the first step. I see it as another tool for people who've already done a lot of the right things and still want to move more money into tax-free accounts. If you've reached that point, this strategy deserves a serious look.

Why I Like the Mega Backdoor Roth

I've always said I'd rather pay tax on the seed than the harvest. Every time I've run the numbers over the last 25 years, I come back to the same conclusion. If you're building meaningful wealth and earning strong investment returns, tax-free growth becomes more valuable every single year. I'm always looking for opportunities to build larger tax-free buckets.

The Mega Backdoor Roth allows eligible investors to move significantly more money into Roth accounts than a Roth IRA alone. For 2026, the total contribution limit inside a qualified defined contribution plan is $72,000 before catch-up contributions, which creates the opportunity to move substantially more money into Roth accounts than a traditional Roth IRA alone. Over the course of 20 or 30 years, that can translate into a solid amount of qualified tax-free growth and qualified tax-free income during retirement.

I'm not chasing another deduction today. I'm creating more flexibility tomorrow.

Does Your 401(k) Even Allow It?

Here's where people usually hit their first obstacle. The Mega Backdoor Roth only works if your 401(k) plan allows after-tax employee contributions. That's the feature that makes the strategy possible. Unfortunately, not every plan offers it. That's why one of the first questions I tell people to ask their plan administrator is "Does my 401(k) allow after-tax employee contributions?" If the answer is no, the strategy probably isn't available through that particular plan.

If you own your own business, you may have opportunities employees don't. With a properly designed Solo 401(k), you have much more control over how your retirement plan is structured. Instead of being limited by whatever plan your employer offers, your plan documents can include the provisions necessary to allow after-tax contributions and support a Mega Backdoor Roth strategy.

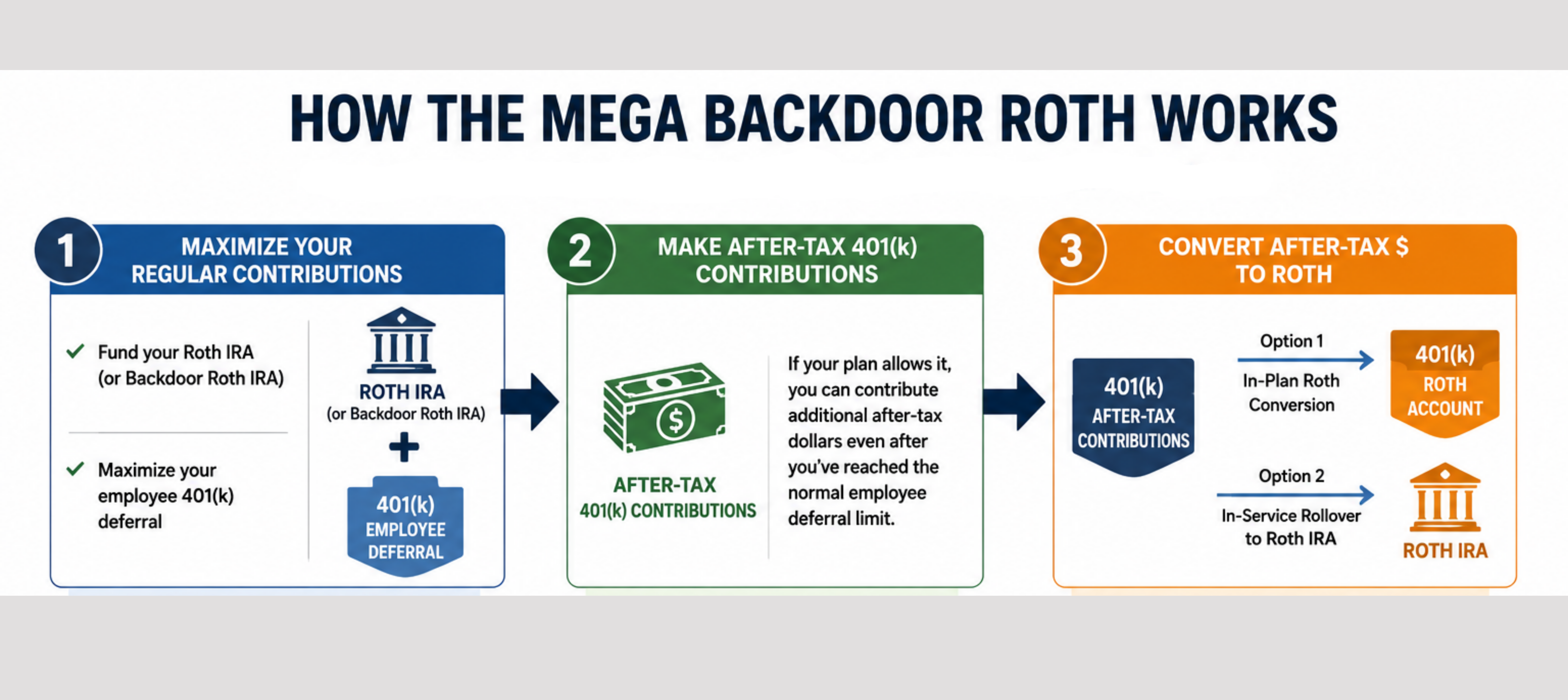

How the Mega Backdoor Roth Works

Once you've confirmed your retirement plan supports the strategy, the process is actually pretty straightforward.

- First, maximize your regular retirement contributions. For many business owners, that starts with funding your Roth IRA or Backdoor Roth IRA and making the maximum employee contribution to your 401(k).

- Next, make additional after-tax 401(k) contributions. If your retirement plan allows it, you can continue contributing after-tax dollars even after you've reached the normal employee contribution limit. This is the feature that makes the Mega Backdoor Roth possible.

- Finally, convert those after-tax dollars to Roth. Depending on how your retirement plan is written, those after-tax contributions can be moved into Roth assets through an in-plan Roth conversion or an in-service rollover to a Roth IRA. That's where the "mega" comes from. You're simply using the after-tax contribution feature to move more money into tax-free accounts than traditional Roth contribution limits would otherwise allow.

Before you get too excited, remember that not every 401(k) plan offers these features. Many employer-sponsored plans don't allow after-tax contributions or in-service Roth conversions, so you'll want to verify what's available before assuming you can use the strategy.

Business owners have another advantage here. If you have a properly drafted Solo 401(k), you can build these provisions right into your plan documents instead of being limited by whatever retirement plan your employer offers.

Common Mistakes to Avoid

Like any advanced retirement strategy, the Mega Backdoor Roth comes with rules. The strategy itself isn't complicated, but I see people make mistakes because they assume every retirement plan works the same way.

The first mistake is confusing a Backdoor Roth IRA with a Mega Backdoor Roth. They're two completely different strategies. A Backdoor Roth IRA helps high-income earners get around the Roth IRA income limits by making a non-deductible IRA contribution and then converting it to a Roth IRA. The Mega Backdoor Roth uses after-tax contributions inside a qualified 401(k) plan to move substantially more money into Roth accounts. Same goal. Different strategy.

Another common mistake is assuming every employer-sponsored 401(k) allows it. As we discussed earlier, only a percentage of plans offer the after-tax contribution feature that's required. That's why your first phone call should be to your plan administrator, not YouTube.

Finally, don't assume that simply because you own a business, the strategy automatically works for you. A Solo 401(k) has to be drafted correctly to include the provisions necessary for a Mega Backdoor Roth. Having the right retirement plan documents matters just as much as understanding the strategy itself.

Is the Mega Backdoor Roth Right for You?

The Mega Backdoor Roth isn't for everyone, and that's perfectly okay.

If you're just getting started with retirement planning, I'd rather see you consistently fund your Roth IRA, take advantage of your employer match, maximize an HSA if you're eligible, and make sure you're using the right retirement plan for your business. Those strategies alone can build tremendous wealth over time. But if you've already built that foundation, have strong cash flow, and you're looking for another opportunity to create more tax-free wealth, the Mega Backdoor Roth deserves serious consideration.

I've always looked at retirement planning as a progression. You don't jump straight to the advanced strategies. You build one layer at a time. As your income grows, your business grows, and your wealth grows, your retirement strategy should grow with it. The Mega Backdoor Roth is simply another tool that helps you continue moving in that direction.

The Bottom Line

The Mega Backdoor Roth is still one of the most effective ways eligible investors can move substantially more money into Roth accounts and build a larger source of tax-free wealth for the future.

The biggest mistake isn't failing to use the strategy. It's assuming it's the first place you should start. Build your retirement foundation first. Take advantage of the opportunities already available to you. Then, when you've reached the point where you're asking how to create an even bigger tax-free bucket, the Mega Backdoor Roth may be exactly what you're looking for.

If you're ready to explore a Mega Backdoor Roth, the first step is making sure your 401(k) plan actually supports the strategy. My team at Directed IRA can help you determine whether your current plan qualifies or whether a properly designed Solo 401(k) would be a better fit. Book a free 15-minute call to discuss your options and start building a larger tax-free bucket.

The best retirement plans don't happen by accident. They're built one smart decision at a time.