S-Corporation format can provide you with some amazing benefits, but if you don’t maintain it properly, you can have a lot of unexpected problems.

I wish that it was as easy as just filing a form with the State. Then you have magical tax savings and bulletproof asset protection, but that’s simply not the case. In order to maintain an S-corporation it is more than that.

The reality is that the tasks can be easy and fairly affordable. Here are the items to check off on your “to-do list” when it comes to maintaining your entity. You’ll truly reap some tax benefits and have a serious level of asset protection.

Here is Your ‘To-Do-List’ of 7 things to be Aware of if You Want to PROPERLY Maintain Your S-Corporation:

.

1. Corporate Documents

Review your initial set-up and make sure you have all of the key components of a proper formation; i.e. Articles, Bylaws, Minutes, Stock Certificates, Corporate Seal, etc… Remember it’s not just ‘filing with the State’ that creates a proper entity.

In fact, it’s surprising how many new clients I meet with that “think” they have an S-Corporation. Come to find out they never filed their S-Election (Form 2553) or they are out of compliance with the Secretary of State. This puts a major dagger into the heart of your S-Corporation Strategy.

2. Annual Minutes and Board Meetings

It’s easy and affordable to make sure you hold your annual Shareholder and Director meetings. It’s also a great write-off opportunity!! Along with that it’s critical for asset protection. Many people think that because I have an LLC ‘taxed as an S-Corp’ I can skip this important step. Don’t do it!!

If you haven’t done your ‘Minutes’ in a few years, all is not lost. Complete what we call a ‘clean up’ and get on a system. Check out our CMP program at KKOS Lawyers and let your Paralegals take care of the details.

3. Annual State Secretary of State Filings

Every state has a different filing fee and procedure for renewing your S-Corporation each year. If you don’t complete this filing, your corporation can be involuntarily dissolved and now you have nothing.

You default to operating as a sole-proprietorship and the IRS can even take issue with your tax filings and disallow your tax filing if you aren’t in good standing with the State.

4. Regular Operations and ‘Using the Name’

To ensure much stronger asset protection in the event of a lawsuit, get into the habit of using your corporate name on all of your legal documents, advertising material, website and certainly your business cards. Let the world know you have incorporated.

Also, if you want the asset protection of an S-Corporation you have to let your customers, vendors and contacts know that ‘your company’ is the one doing business. You are simply an officer and employee of the corporation.

5. Quarterly Payroll

Setting up your personal payroll procedure is the most critical aspect of owning and operating an S-Corporation to save taxes.

This process includes making sure you have a proper payroll level established for you that is realistic and not to aggressive yet allows for maximum self-employment tax savings. Next, it requires that you file quarterly payroll reports and making deposits based on your particular situation.

The deposits vary based on the amount of your payroll. Choosing the proper payroll is absolutely critical.

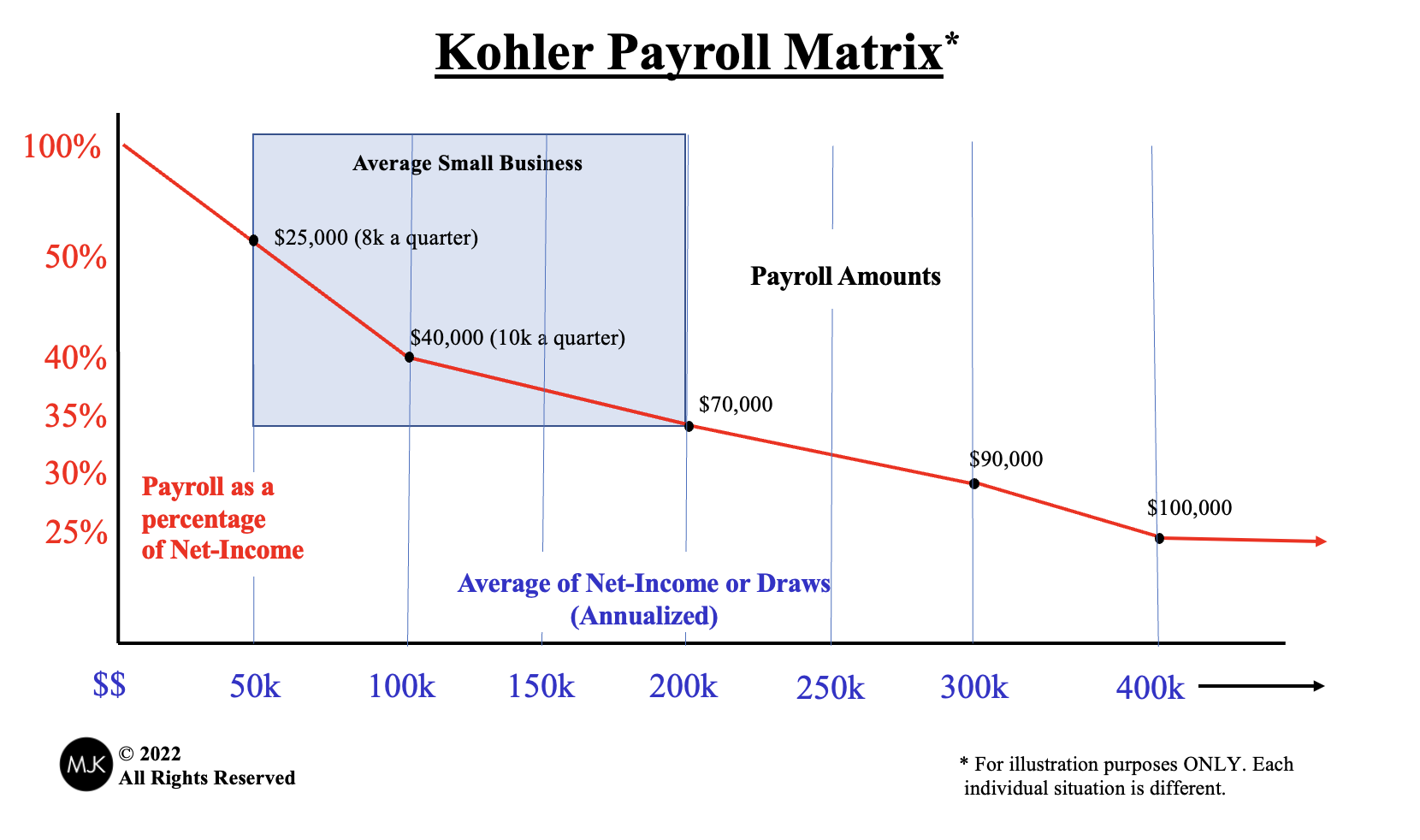

Here is a diagram I have referred to as the “Kohler Payroll Matrix” over the years. This is an updated version since the passing of the Tax Cuts and Jobs Act effective in 2018, and can be a useful visual guide in determining the proper salary level in your S-Corporation from year to year.

You’ll see that I begin the diagram at $50,000 of net income and a 50 percent payroll allocation at that level. As such, when taking the operational costs of to maintain an S-Corporation into account, it typically doesn’t make sense to utilize the S-Corporation unless you’re making a net income of at least $40,000.

MOST IMPORTANTLY, note that determining the proper payroll for a business owner is not an absolute science. It’s a subjective analysis and this diagram is simply a ‘starting point’ or a ‘guide’ for S-Corporation owners to talk about with their tax professional. Nonetheless, I have found these boundaries to be sufficiently reasonable in discussions with IRS representatives when working with clients and their payroll allocation over the past 20 years.

6. Tax Return Filing

It’s well recognized that S-Corporations provide incredible audit protection. It is also estimated they are audited up to 15x less frequently than that of Sole-proprietorships. However, if you don’t file your tax returns on time and/or an extension, you will actually increase your chances of an audit dramatically and the penalties for late filing have gone through the roof.

The required tax return is an 11020-S and is due by March 15th…UNLESS you file an Extension you have until September 15th to file the final return.

7. State Tax Filing Requirements

Every state is a little different when it comes to S-Corporation filing requirements. Some states are cheap and easy, others are expensive and complex, with of course everything in between. Familiarize yourself with your State’s rules and get set up on a system with your accounting professional.

Conclusion

Bottom line, the S-Corporation can be a powerful structure and tool to save on self-employment taxes. Additionally, it can protect a business owner’s personal assets from lawsuits that may arise from their operations. Keep in mind that all of this comes with an administrative cost.

Make sure you are familiar with your responsibilities as an owner of this incredible small business tool.