Short-term rentals continue to be one of the most tax-advantaged real estate investments available, but they're also one of the most misunderstood. Unlike traditional rental properties, short-term rentals follow a unique set of IRS rules that can affect where you report the income, whether you owe self-employment tax, and whether your rental losses are treated as passive or ordinary.

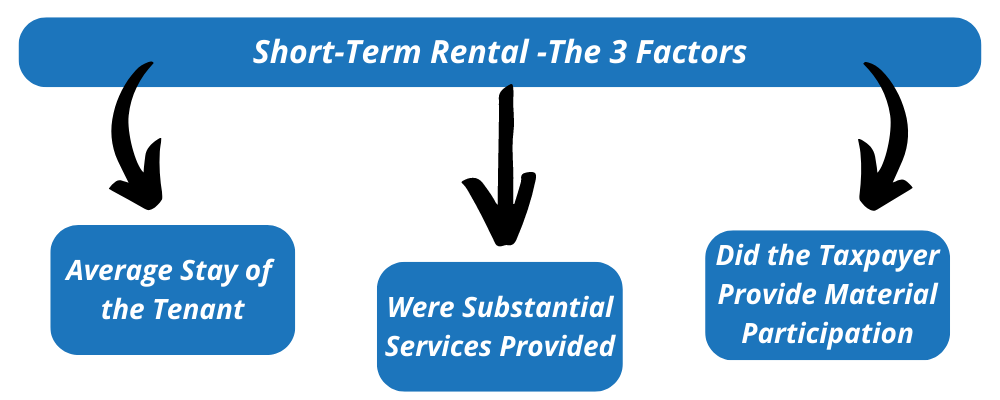

That's why understanding how short-term rentals are taxed is so important. With the right planning, you may be able to maximize deductions while avoiding common mistakes that can cost you thousands. The key is understanding three factors: your average rental period, the services you provide to guests, and whether you materially participate in the activity.

What Does the IRS Consider a Short-Term Rental?

For tax purposes, not every Airbnb or vacation rental is treated the same. The IRS looks at three primary factors to determine how your short-term rental will be taxed:

- The average number of days each guest stays at the property.

- Whether you provide substantial services during your guests' stay.

- Whether you materially participate in the operation of the rental.

Those three factors determine whether your rental income belongs on Schedule E or Schedule C, whether it's subject to self-employment tax, and whether you may qualify for ordinary loss treatment.

As a result, short-term rentals generally fall into one of four categories:

-

- Business short-term rental with material participation

- Business short-term rental without material participation

- Passive short-term rental with material participation

- Passive short-term rental without material participation

Let's walk through each factor.

1. Average Rental Days a Guest Stays at the Property

The first question is: How long does the average guest stay at your property? The IRS uses the average length of stay over the course of the year, not the length of any individual reservation. To calculate your average stay, divide the total number of rental days by the total number of guest stays.

EXAMPLE: You rent your cabin to 21 different groups throughout the year for a total of 108 rental days.

108 ÷ 21 = 5.14 average days per stay

Since the average stay is fewer than seven days, your property falls under the IRS's short-term rental rules.

-

- If the Average Stay Is Less Than Seven Days: You may report the activity on Schedule E, just like a traditional rental property. The income generally is not subject to self-employment tax, and you may qualify for ordinary loss treatment if you also materially participate in the activity.

- If the Average Stay Is More Than Seven Days: You may still report the activity on Schedule E, and the income generally is not subject to self-employment tax. However, the opportunity to convert rental losses into ordinary losses under the short-term rental rules generally is no longer available.

The next question is whether the services you provide rise to the level of the IRS's definition of "substantial services." There are pros and cons to providing substantial services. It can affect your rental rates as well as the tax consequences.

2. Substantial Services and a Business Short-Term Rental

The IRS has deemed that if you provide substantial services to your guests, then the income you make needs to be reported on a Schedule C, the end. This essentially means you have a business short-term rental. You’ve elevated your activity to that of a business (think of it like a hotel).

-

- If You Provide Substantial Services: The activity is generally reported on Schedule C, and any net income is subject to self-employment tax. Depending on your overall tax strategy, an S corporation may help reduce that tax burden.

Keep in mind that reporting the activity on Schedule C does not automatically qualify you for ordinary loss treatment. Material participation is still required.

Examples of substantial services include:

-

-

- Daily housekeeping while the same guest occupies the property

- Changing linens during the guest's stay

- Concierge services

- Guided tours or excursions

- Providing meals, such as breakfast each morning

- Transportation services

- Other hotel-style services

-

By contrast, amenities such as Wi-Fi, utilities, routine maintenance, trash service, or cleaning between guest stays generally are not considered substantial services.

-

- If You Do Not Provide Substantial Services: You may generally continue reporting the activity on Schedule E, the income is not subject to self-employment tax, and you may still qualify for ordinary loss treatment if you materially participate.

The IRS has provided limited guidance on where the line is drawn, so it's important not to assume that adding premium guest services automatically creates a tax benefit. In some cases, providing too many services can actually produce a negative tax result.

3. Material Participation

This is where short-term rentals become especially valuable from a tax planning perspective.

Unlike most rental properties, qualifying short-term rentals may allow rental losses to be treated as ordinary losses rather than passive losses if you materially participate in the activity.

The IRS provides seven tests for material participation, but you only need to satisfy one of them, not all seven. While all seven tests carry equal weight under the tax code, we've found over the years that most investors who qualify do so under one of the first three tests. Those tend to be the most straightforward to document and apply in practice.

The seven material participation tests are:

- You participate in the activity for more than 500 hours during the year.

- Your participation constitutes substantially all of the participation in the activity by everyone involved.

- You participate in the activity for more than 100 hours during the year, and no one else participates more than you do.

- The activity is a significant participation activity, and your combined participation in all significant participation activities exceeds 500 hours for the year.

- You materially participated in the activity for any five of the previous ten tax years.

- The activity is a personal service activity, and you materially participated in the activity for any three prior tax years.

- Based on all the facts and circumstances, you participate in the activity on a regular, continuous, and substantial basis.

Because material participation is based on your actual involvement, it's important to keep accurate records of the work you perform throughout the year. Maintaining a detailed log of your time and activities can make all the difference if the IRS ever questions your participation.

How It Works

If you qualify under any one of the seven material participation tests, a net loss from a qualifying short-term rental may be treated as an ordinary loss rather than a passive loss. This means the loss may be used to offset other sources of income on your tax return, making short-term rentals one of the most powerful tax planning opportunities available to active real estate investors.

This strategy becomes even more valuable when paired with a cost segregation study, which can accelerate depreciation and significantly increase your first-year deductions.

While the IRS rules governing short-term rentals were written long before platforms like Airbnb and Vrbo became commonplace, the strategy remains available today. The key is making sure you can properly support your position with accurate records and documentation if your return is ever questioned.

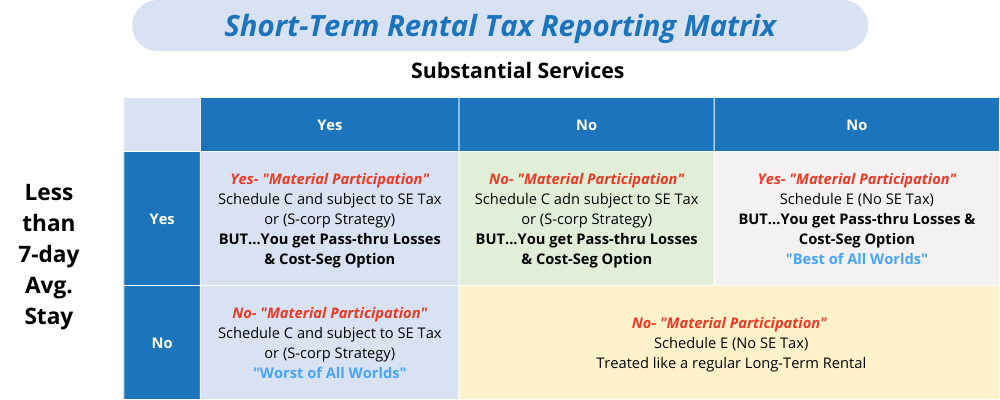

The Short-Term Rental Taxation Matrix

When determining how your short-term rental will be taxed, it's helpful to look at all three factors together:

-

- Your average rental period

- Whether you provide substantial services

- Whether you materially participate in the activity

These factors determine whether your rental activity is reported on Schedule E or Schedule C, whether the income is subject to self-employment tax, and whether you may qualify for ordinary loss treatment.

The following matrix summarizes how the different combinations of these rules affect the taxation of your short-term rental.

Notice that material participation is one of the most important variables in the analysis. It's what creates the opportunity for qualifying short-term rental losses to be treated differently than losses from most traditional rental properties.

Short-Term Rentals Reported on Schedule E

If you do not provide substantial services, your short-term rental will generally be reported on Schedule E, just like a traditional rental property.

One of the biggest advantages of Schedule E treatment is that your rental income generally is not subject to self-employment tax.

That doesn't mean you can't provide amenities or conveniences for your guests. In fact, many services are considered customary for rental properties and do not rise to the level of substantial services.

Examples include:

-

- Heating and air conditioning

- Water and gas

- Internet and Wi-Fi

- Cleaning common areas

- Routine repairs and maintenance

- Trash collection

- Payment of HOA dues

These types of amenities help maintain your property and improve your guests' experience without converting your rental activity into a hospitality business.

Personal Use of the Property

Owning a vacation rental doesn't prevent you from using it yourself, but personal use can affect the property's tax treatment.

Generally, you can maintain the property's status as a rental if your personal use does not exceed the greater of:

-

- 14 days during the year, or

- 10% of the total days the property is rented to others at fair market value.

It's also important to distinguish between personal use days and work days.

If you're staying at the property to perform legitimate repairs, maintenance, improvements, inspections, or other management activities, those days generally are not considered personal use. Keep detailed records of the work you perform, including dates, receipts, and notes describing the tasks completed.

Those work trips can also create additional tax deductions for qualifying travel expenses, meals (when applicable), vehicle expenses, and supplies related to maintaining the property.

The key is having documentation that clearly supports the business purpose of your visit.

The Bottom Line

Short-term rentals offer tax advantages that simply aren't available with most traditional rental properties. Understanding how the IRS treats average rental periods, substantial services, and material participation can help you structure your investment properly and take advantage of opportunities to reduce your tax liability.

Not sure how these rules apply to your short-term rental? A Main Street Certified Tax Pro can help you determine the right reporting method, identify tax-saving opportunities, and make sure you're taking advantage of every deduction available under the law. Find a Main Street Certified Tax Pro today and put a tax strategy in place that works as hard as your investment. Explore Main Street Certified Tax Pros from across the country, each personally trained and certified by me to speak the same tax language and deliver the proactive strategies I teach.

Because these rules are highly technical, even small mistakes can have significant tax consequences. A little planning upfront can help you avoid unnecessary taxes, maximize available deductions, and build a stronger long-term investment strategy.