One of the most common questions I get from real estate investors is, "How many rental properties should I put in one LLC?"

The answer is…it depends.

I know that's not the answer you were hoping for, but hear me out. The right answer isn't based on the number of properties you own. It's based on the amount of equity you're protecting, the level of risk each property carries, and where those properties are located.

I've seen investors make both extremes of this mistake. One client owned 42 rental properties with more than $2 million in equity, all inside a single Arizona LLC. Later that same day, I met another client who owned just four properties with very little equity, each in its own Nevada LLC even though they lived in California. Both situations were expensive mistakes that needed fixing.

Asset protection doesn't have to be all or nothing. With the right planning, you can protect the equity you've built without paying to maintain LLCs you don't need.

Why Should You Put Rental Properties in an LLC?

An LLC is one of the best asset protection tools available to real estate investors.

When properly formed and maintained, an LLC helps separate your personal assets from the liabilities associated with your rental properties. If someone is injured on one of your properties or files a lawsuit against your rental business, the LLC creates a layer of protection between that claim and your personal wealth.

LLCs also offer flexibility from a tax perspective. Most rental property LLCs are taxed as pass-through entities, meaning the income and expenses flow directly onto your personal tax return. You still receive the benefits of deductions such as depreciation, repairs, maintenance, insurance, and other operating expenses without the double taxation associated with traditional corporations.

Beyond the legal and tax benefits, operating your investments through an LLC creates a cleaner, more professional structure that becomes increasingly valuable as your portfolio grows.

Should Every Rental Property Have Its Own LLC?

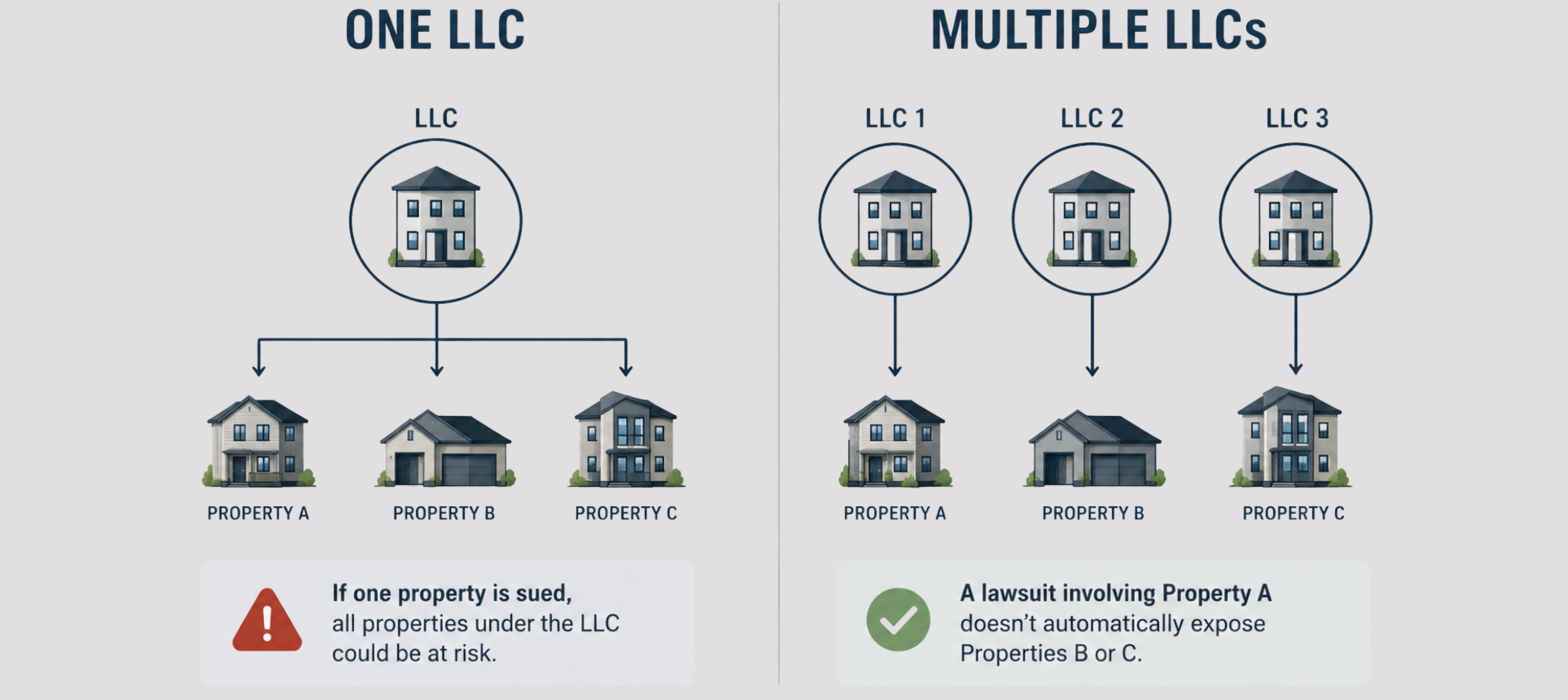

Not necessarily. This is probably the biggest misconception I hear from real estate investors. Some people assume every rental property deserves its own LLC, while others put every property they own into a single entity. In reality, both approaches can create unnecessary problems.

Every additional LLC comes with formation costs, annual fees, tax filings in some states, bookkeeping requirements, and administrative work. Creating separate entities for every property may provide excellent liability protection, but it can also become expensive very quickly.

On the other hand, putting every property into one LLC creates a different problem. If one property becomes involved in a lawsuit, every property owned by that LLC could potentially be exposed. Finding the right balance is where good planning makes all the difference.

Don't Count Properties. Count Equity.

When clients ask me how many properties belong in one LLC, I don't start by counting properties. I start by looking at equity.

A rental property with $40,000 in equity creates a very different risk profile than one with $800,000 in equity. The number of doors isn't nearly as important as the amount of wealth you're putting at risk.

As a general rule of thumb, I begin looking closely at separate LLCs once a property has accumulated significant equity, often somewhere around the $200,000 mark. That's not a hard-and-fast rule, but it's a useful starting point for evaluating your asset protection strategy.

Every investor's situation is different, which is why your LLC structure should be built around your portfolio instead of applying the same formula to everyone.

When Should a Property Have Its Own LLC?

Certain situations make separate LLCs much easier to justify. High-equity properties are usually the first candidates. The more equity a property has, the more attractive it becomes to a plaintiff's attorney. Isolating those properties can help prevent one lawsuit from putting your entire portfolio at risk.

Property type also matters. A short-term rental generally carries more liability than a long-term residential rental because you have a much higher turnover of guests. Commercial properties may present different risks than single-family homes or duplexes. As the risk profile changes, your entity structure should change with it.

Ownership is another consideration. If different partners own different properties, separate LLCs often make bookkeeping, liability, and ownership much cleaner.

Does It Matter Which State Your Rental Property Is In?

Absolutely. Real estate is governed by state law, and each state has its own filing requirements, fees, and compliance rules.

If you own rental properties in multiple states, it often makes sense to organize them by state rather than forcing everything into one entity. For example, if you own three rentals in Florida and two in Texas, creating one Florida LLC and one Texas LLC may simplify compliance while still providing strong asset protection.

Trying to force properties in multiple states into one structure can create unnecessary filings and additional costs.

Should You Consider a Series LLC?

A Series LLC can be an excellent option in certain states, but it isn't available everywhere.

States like Texas and Delaware allow investors to create separate "series" under one master LLC. Each series can own its own property while maintaining liability protection from the others. This can reduce filing costs and simplify administration compared to maintaining multiple stand-alone LLCs.

However, Series LLCs aren't recognized in every state, and lenders, title companies, and attorneys don't always treat them consistently. Before using one, it's important to understand how your state handles Series LLCs and whether they're the right fit for your investment strategy.

The Biggest Mistake Real Estate Investors Make

The biggest mistake isn't having too many or too few LLCs. The biggest mistake is building your entity structure without a plan.

I've watched investors spend thousands of dollars maintaining LLCs they didn't need. I've also seen investors expose millions of dollars in equity because they assumed one LLC was "good enough." Neither approach is strategic. Your entity structure should grow alongside your portfolio. As your equity increases, your investments expand, or your goals change, your LLC strategy should evolve with them.

The Bottom Line

There isn't a magic number of rental properties that belongs in one LLC. The better question is whether your current structure is protecting the amount of equity you've built.

Every property, every investor, and every portfolio is different. That's why the best LLC strategy is based on balancing liability protection, administrative costs, and long-term wealth building.

If you're building a real estate portfolio, don't guess when it comes to asset protection. The attorneys at KKOS Lawyers can help you design an LLC structure that protects your investments without creating unnecessary complexity, so your entity strategy grows right alongside your portfolio.

.png?width=6440&height=1438&name=KKOS%20Book%20a%20Call%20(2).png)