Before you rush to file your taxes this April, stop and check your meal deductions. Business owners miss this write-off all the time, and it can easily add up to real money over the course of a year. If you haven't filed yet, you may still be able to capture some of these deductions. And if you want to make sure every business meal you pay for this year actually helps lower your taxes, the rules below will show you exactly how it works.

First, Understand the Basic Rule

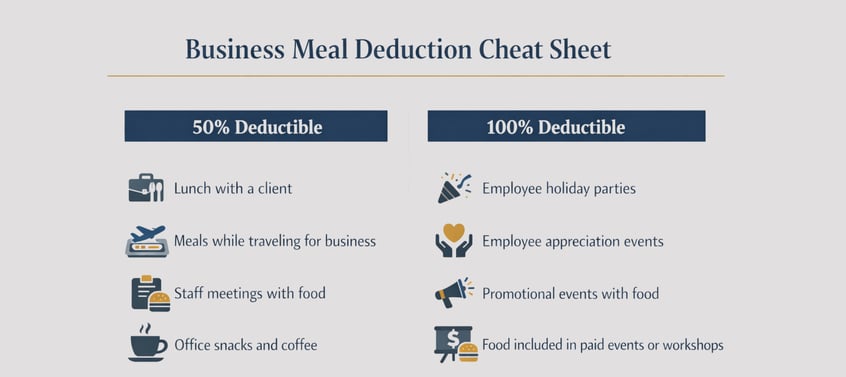

In most situations today, business meals are 50% deductible when they're ordinary, necessary, and directly related to your business.

That means you can usually deduct half the cost of meals when you're:

• Meeting with a client or prospect

• Traveling for business

• Meeting with a vendor or business partner

• Holding a legitimate business discussion over a meal

However, some types of food expenses are still 100% deductible, while others are limited or not deductible at all. The key is understanding the category your expense falls into.

Type 1: Dining With a Prospect or Important Client

Meals with a customer, client, prospect, or business partner are one of the most common business meal deductions.

If you meet a client for lunch and discuss business, 50% of that meal is generally deductible.

The key requirements are:

• The expense must be ordinary and reasonable

• You or someone from your business must be present

• Business must be discussed before, during, or shortly after the meal

Be sure to document the who, what, where, and why of the meeting in your records.

Type 2: Meals While Traveling for Business

Meals while traveling overnight for legitimate business purposes are also 50% deductible.

This includes meals while attending:

• Conferences or training events

• Board meetings or retreats

• Trips to check on rental property

• Travel to meet clients or vendors

You don't need to have a client with you. Even meals eaten alone while traveling for business qualify as long as the travel itself is legitimate. Your deduction includes the meal, tax, and tip.

Type 3: Meals With Employees or Staff Meetings

If you take employees out for a meal or order food during a staff meeting, the meal is typically 50% deductible.

Examples include:

• Lunch during a team meeting

• A planning session with employees

• A working lunch with staff

If the meal is primarily for employees and business discussion is taking place, it generally falls into this category.

Type 4: Food in the Office Kitchen

Food provided in the office kitchen for employees is also generally 50% deductible.

Examples include:

• Coffee and beverages

• Snacks or treats for employees

• Office kitchen supplies

These expenses used to be fully deductible years ago, but under current tax rules they're now typically limited to 50%. Please make sure to note that these expenses must be for employees, not for the business owner personally.

Type 5: Employee Parties and Team Events

Some food expenses are still 100% deductible, and this is one that business owners don't even think about.

Food and entertainment for employee events such as holiday parties or team-building activities are fully deductible as long as the event is primarily for employees and not just for owners or highly compensated individuals.

Examples include:

• Holiday parties

• Summer employee appreciation events

• Team-building activities

These events remain one of the few situations where food expenses are still fully deductible.

Type 6: Marketing Events or Promotional Activities

Food expenses connected to marketing or promotional events can also be 100% deductible.

Examples include:

• Snacks at a real estate open house

• Food at a free seminar or workshop

• Refreshments at a promotional event

• Food included as part of a paid training or conference

In these cases, the food is considered part of the marketing or promotional activity, not a traditional meal expense.

Substantiating Your Expenses

Because meal deductions have different percentages depending on the situation, it's important to track them carefully.

I recommend creating separate bookkeeping categories for different types of meal expenses in your accounting software. This makes it much easier to calculate the correct deduction and substantiate the expense if questions arise later.

At a minimum, you should track:

• Meals with clients or prospects

• Travel meals

• Employee meals or staff meetings

• Office kitchen food

• Employee events

• Marketing or promotional food

Keeping these categories organized throughout the year makes tax preparation significantly easier.

If You Haven't Filed Yet

If you haven't filed your tax return yet, take a moment to review your records for meal expenses you might've missed.

Business owners overlook legitimate deductions because they didn't categorize the expenses correctly during the year. Reviewing your credit card statements and business accounts usually uncover additional deductions before filing.

Planning for the Rest of the Year

If you've already filed your return or missed some deductions, don't worry. The most important step now is to start tracking these expenses properly going forward. Make sure your bookkeeping system clearly separates meal categories and that you document the business purpose of each expense. Doing this consistently throughout the year makes tax time far easier and ensures you capture every deduction you're entitled to.

The Bottom Line

Business meals can add up to a meaningful deduction, but only if you actually track them. Too many business owners miss these write-offs because their bookkeeping is messy or incomplete.

If you've already missed out on food and meal deductions for the 2025 tax year, NOW is the time to get your bookkeeping in order and lock in these write-offs for 2026. Don't have time to track receipts and expenses? Try Xero, a simple cloud-based bookkeeping platform that helps you track expenses, categorize meals, and keep your records clean all year long. For a limited time, you can sign up with this link to get 90% off your first six months of Xero. It's one of the easiest ways to stop losing deductions and save yourself from the tax-season headaches.